The Richest Investor in Babylon (Book-in-Book)

4,000 years ago a Babylonian asked a rich person to mentor him. This wealthy man slowly taught him the main rules to the real estate investment, which live out of time and that anyone can apply.

Inspired by the all-time classic book by George S. Clason - "The Richest Man in Babylon".

The main book "Quantum REI Analysis" has this book-in-book "The Richest Investor in Babylon" as one of its chapters.

Difficulty: hard. 30 min read.

Table of Contents

Book-in-Book Summary

A contemporary archaeologist reveals 5 Babylonian clay tablets. They baked and became a hard tile. They reached about four by eight inches and one inch thick:

{kind=link}

These parables tell about ancient Babylon. Specifically, set 4,000 years ago.

A fictional Babylonian character called Bel tells parables. He works as a construction estimator who became "the richest investor in Babylon."

Basically, Bel asks a rich person Abu-Waqar to mentor him. Abu-Waqar scolds the construction estimator when he makes mistakes, but eventually the devoted disciple gets the richest investor in Babylon.

Clay Tablet 1, Bazaar dog

Acquaintanceship

Abu-Waqar, a wealthy Babylonian, hired Bel, a poor construction estimator.

Abu-Waqar also hired two other estimators. Each of the 3 estimators prepared a different version of the estimate for the future pool in Abu-Waqar' garden:

Abu-Waqar carefully compared the prepared estimates. Bel's estimate looked 2 times cheaper and the work period shortened by half than that of the other estimators. The "Digging the pool" item on Bel's estimate indicated "0 shekels, for 1 day." Abu-Waqar asked for an explanation. Bel explained in detail.

Digging a hole for a pool takes half the time and half the cost of construction. The contractor must remove the excavated ground outside of Babylon. Removal of the ground costs a lot of money. Babylon's houses restrict the streets, and a lot of traffic prevents fast movement. Traffic decreases in the evening. But the king's guards close the Ishtar Gate at sunset:

After that, no powerful magical spell can open the gate before sunrise.

Bel heard that the king's chief gardener wanted to build another hanging garden:

Babylon had many houses and no open space. The nearest land for a garden lay outside the city wall. Bel brought samples of the land from Abu-Waqar' pool to the king's gardener. The gardener approved of the land. The future Abu-Waqar' pool located near the king's hanging gardens. The gardener agreed to excavate the pool and take the ground for himself. He disposed of 60 water carriers. By law, the people of Babylon must give way to the king's porters. Digging the pool and removing the land would take 1 day, and Abu-Waqar had to pay nothing for it.

Abu-Waqar feels admiration. Bel thought about more than just preparing an estimate. Abu-Waqar paid for the estimate and asked what else he could do to help the estimator. Bel asked him to tell what actions lead to wealth. Surprise filled Abu-Waqar. Usually, everyone asked him for money. Bel became the first to ask him for knowledge.

Abu-Waqar began to remember. He, too, had money problems as a young man. And just like Bel, he needed a mentor. Abu-Waqar agreed to help the estimator.

First task

Abu-Waqar advised Bel to go to the bazaar and listen to people talk. Bel should find information about people who don't pay their creditors and have other problems with money.

Within a week Bel collected information about 12 Babylonians who had money problems. Some of them had taken money for a business and failed, and others had used a loan for entertainment, but lost their jobs and couldn't pay it back, and the others had lost their money at dice.

A trusted mentor assistant met with all of them. One of the 12 agreed to sell his house cheaply and get the money quickly. Mentor Abu-Waqar paid, repaired the house, and sold it. Bel received 1/60 [or 1.7%] of the value of the repaired house.

Bel understood the value of information about houses whose owners needed money.

Accumulation of information sources

The mentor advised to get to know the moneylenders, the servants in the caravanserais where gambling didn't stop even at night, the scribes who wrote the loan contracts,... They provided information about people who needed money:

- Problems with credit

- Recent legacy.

- A big dice loss

- ...

Accumulation of regular buyers

The mentor also asked Bel to make contacts among people willing to buy houses quickly at an inexpensive price:

- Trading houses

- Rich people

- Builders

Bel found several people who regularly handled "low-cost buy-repair-market sales" type deals. Bel negotiated that they would pay Bel 1/60 [or 1.7%] of the property value after they repaired and sold it on the market. This relieved Bel of his dependence on his mentor.

Reliability of bazaar-dog income

Bel feared that buyers would sell the renovated property that Bel found, but would not pay him 1/60 [or 1.7%] of the value of the house after the sale.

Abu-Waqar reassured Bel. Buyers earn ten to twenty times more on the resale of a renovated house. They will gladly pay Bel a small portion of the proceeds from the profits made. If buyers hide some repairs-sales from him, Bel will no longer provide them any information. The cheating buyer will lose a regular source of suitable homes.

The mentor thought Bel needed to see another difference between buyers. The buyers had different activity. He should look for the most active buyers who worked hard with each of Bel's properties.

When Bel found a new suitable buyer, he gave him information about suitable houses for an entire month. At the end of the month, Bel counted how much money he received from the new buyer. If the buyer showed no activity and gave Bel little money, Bel wouldn't work with him anymore.

Full-time work

Soon Bel had several regular buyers. They actively worked with the property owners and accurately paid for the information. Some of the regular buyers even invited Bel to attend the sale of the renovated house. They paid Bel immediately after the sale of the house.

Bel knew well the preferences of regular buyers. He provided property information to the buyer who preferred a similar type of property.

Bazaar-dog income became enough to live on. Bel stopped working as a construction estimator and switched completely to information searches. Now new regular buyers came to Bel on their own. They asked to report on found homeowners who needed money.

Clay Tablet 2, Rule of 2/3

Naive rule of wealth

Bel told the мentor that his friend Bansir saves 1/12 [or 8%] of his income and plans to give credit. Bel started saving money, too.

Abu-Waqar laughed for a long time. He said that the more popular the rule, the worse it works. Popular rules look very simple to attract as many people as possible. But when everyone uses a popular rule, it loses value. Everyone can't turn into rich people.

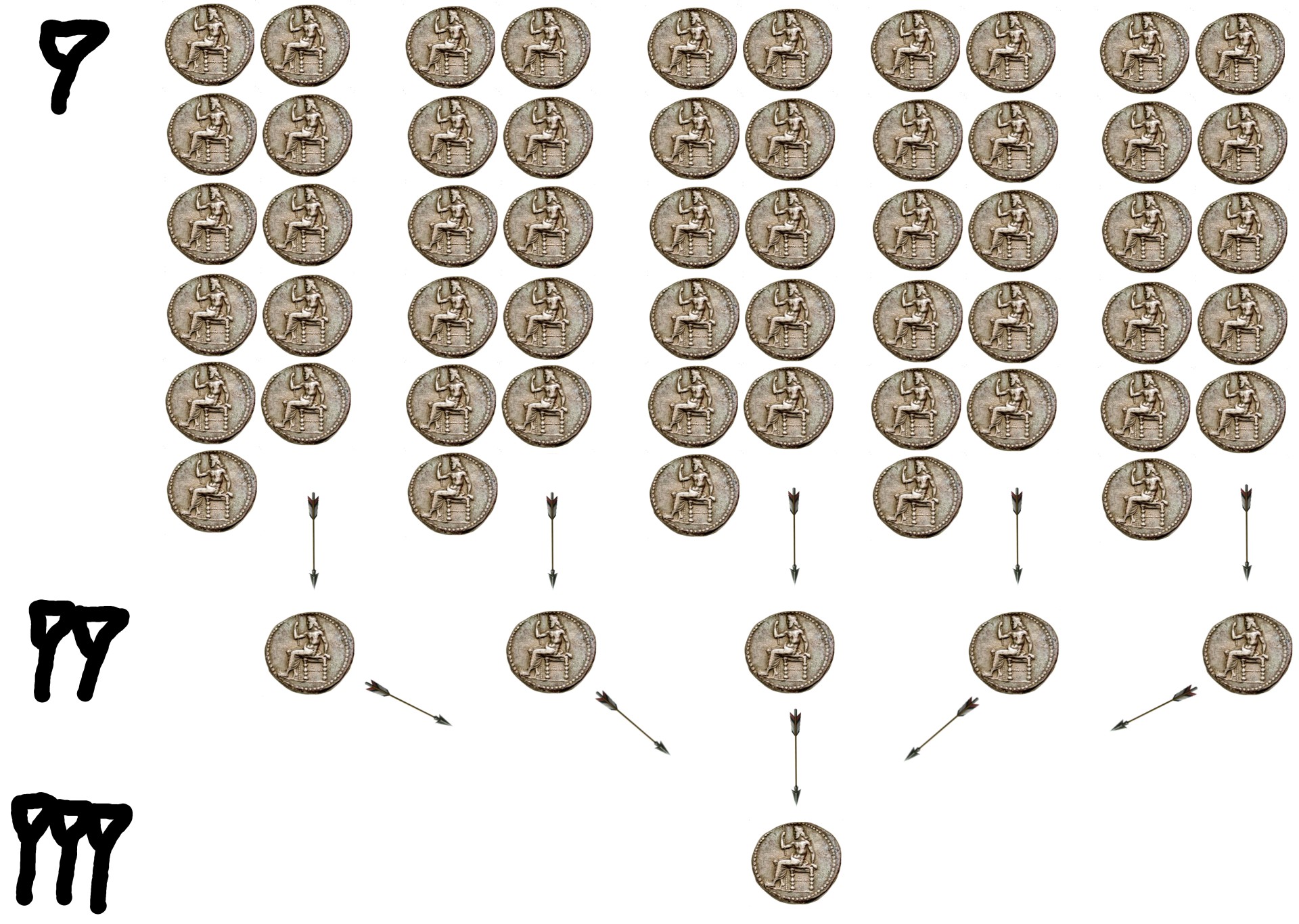

The naive 1/12 [or 8%] rule targets people who can only count to 12. The rule has three simple steps. At the first step you need to earn money and set aside every 12th silver shekel. In step two you need to accumulate 5 silver shekels and give them in growth. In step three you must wait one year and receive 1 silver shekel:

Babylon overflows with inspired teachers of wealth. They teach everyone who wants to find wealth. The wealth seeker may not even know how to count to 12. Potters in bazaars sell clay tablets with this scheme. The tablet costs one silver shekel, and contains a recess for each coin. Potter explains in detail how to fill the tablet with coins. He can even name a couple of acquaintances who bought this tablet from him and became rich. The seeker has to fill in the empty spaces with coins and dream of becoming rich.

Abu-Waqar pointed out a problematic aspect of this way of accumulating wealth. A mountain of 60 silver shekels in a year brings an income of 1 silver shekel. Bel must wait decades for the income from the loan to become sufficient to live on. Usually, this scheme stops at step 2. It's enough that Bel loses his job for a month or someone in the family gets sick. Then he would have to spend the savings.

The mentor advised Bel to spend all of his bazaar-dog income on himself. Bel could not have accumulated great wealth by adding a share of his small wealth anyway. He can accumulate wealth by regularly adding a share of someone else's great wealth. But to do that, Bel has to do a good count of other people's wealth and use more sophisticated rules than the little naive 1/12 rule.

Maximum purchase price

Bel's training took on a new level. Bel now had to calculate the proposed price for the house.

The mentor asked Bel for another property:

- To make an estimate for repairs

- To find out the value of similar neighboring homes

- To determine the approximate value of the troubled home after repairs.

Bel soon brought all the necessary information. Abu-Waqar opened the "Rule of 2/3" [or 67%]. The combined cost of purchase and the cost of repairs must not exceed two-thirds of the cost of a typical home on the market:

Purchase + Repair ⩽ 2/3 of the cost after repair

[Purchase + Repair ⩽ 67% of the cost after repair]

From there Bel calculated the maximum price of the house that he could not exceed in negotiations:

Maximum Purchase Price = 2/3 of the cost after repair - Repair

[Maximum Purchase Price = 67% of the cost after repair - Repair]

Filter owners

The mentor directed Bel to another property owner to negotiate a price. The owner refused; he wanted more than the 2/3 rule allowed. The failure confused Bel. But Abu-Waqar asked him to continue looking for houses, apply the 2/3 rule, and negotiate with the owners.

One by one, the property owners refused to sell their house. Only the 12th owner agreed to sell the house for the purchase price of Bel. Thus came the first victory!

Abu-Waqar paid for the house, repaired it, and sold it at market price. He took 2/3 [or 67%] of the money he received, which he spent on the purchase and repairs . A profit of 1/3 [or 33%] of the value of the repaired house remained. The mentor gave Bel half of the profit and took the other half for himself. Bel received 1/6 [or 17%] of the value after the repairs. This amounted to 10 times the 1/60 [or 1.7%] he received as a bazaar dog.

Bel understood the value of cleaned and processed property information. It' cost a lot more than raw information.

Accumulation of buyers

Abu-Waqar gave the next assignment. Bel started looking for people who needed information about troubled housing and estimates for repairs.

1) Bel questioned all those to whom he provided raw information as a bazaar-dog. Many of them agreed to work on the new terms. They preferred houses with relatively minor repairs to reduce the fallout in an erroneous repair estimate.

2) Buyer-builders preferred homes with elaborate repairs. This reduced the purchase price and increased the value of their repair skills.

3) Bel also searched for acquaintances among the mercantile houses and wealthy people. Many of them wished to exchange their silver for the purchase and repair of houses. They preferred big houses. Buyers invested 2/3 [or 67%] of the value of the house after repairs and made a profit of 1/6 [or 17%] of the value of the repaired house. In one month they made a profit of 1/4 [or 25%] of the money they paid in. If they gave this money on credit, they would have to wait 1 year and 3 months for a similar profit.

Income reliability

Bel suspected that potential buyers might buy the fund house directly to collect Bel's profits at the same time. Bel's mentor advised him to write a contract with the seller. The scribe in the marketplace prepared the contract. The owner agrees to sell the house at a fixed price to Bel or to anyone Bel points out.

The agreement expired one month. The owner had no right to sell the house to anyone else until the contract expired. The owner paid Bel half of the negotiated purchase price for breaking the contract.

Bel could now safely offer a property to many potential buyers at the same time.

Pay the helpers first

Bel began to accumulate extra money. His mentor opened a new rule, "Pay your helpers first." He advised hiring helpers. They would take over some of Bel's work.

Bel started training bazaar-dogs. They looked for information of homeowners who needed money. This freed up Bel's time for more skilled work.

The money started coming in faster. But preparing calculations for the sale and working with buyers took more and more time. Bel hired a familiar construction estimator. The estimator calculated the cost of repairs, the value of the house after repairs, and calculated the maximum purchase price.

Bel focused entirely on negotiating with sellers and buyers. The cash flow accelerated even more.

Bel hired a trusted helper who handled all negotiations with owners and buyers. At last the assistants completely replaced Bel. He could focus more time on his training.

Sales acceleration

Little by little, Bel became well able to understand the requirements of his buyers. His assistant offered the next property first to buyers who preferred this type of property.

7-10 days

Potential home-buyers greatly appreciated the accuracy of Bel's calculations. This increased the credibility of Bel's information and made the decision to buy easier. The large number of potential buyers further accelerated the sale. Bel reduced the contract period from a month to 7-10 days. Fast money increased the owners' interest in selling their property, even at a low price. Already one in six homeowners in need of money agreed to Bel's price.

1 day

Some owners wanted the money in one day. Bel applied the "1/2 Rule" in such cases:

Maximum Purchase Price = 1/2 of the cost after repair - Repair

If the owner agreed, Bel quickly found the money. He knew which prospective buyers always had free money and trusted Bel's estimates. The ultra-fast sale resulted in an additional profit. It amounted to 1/6 [or 17%] of the value of the repaired house. Sometimes Bel shared the extra profit with the buyer, sometimes he kept the extra profit for himself.

Now people with money found Bel on their own and asked to invest their money profitably for up to a month.

Bel resold several houses in one month. From each sale Bel received 1/6 [or 17%] of the price after repairs. A one-day deal brought in 1/3 [or 33%] of the price after repairs. He distributed 1/12 [or 8%] of the value of the house after repair between his assistants and the bazaar-dog. Bel kept the rest of the profit [9 to 25%]. Now each month he accumulated money that he didn't know where to spend it. Bel asked his mentor for advice on how to spend the money better.

Clay Tablet 3. Repair

The training went to the next step. The mentor pointed out to Bel that home-buyers give money to buy/repair, but take 1/6 [or 17%] of the cost after repairs. Bel can make that profit. Bel has to learn how to finance the purchase and organize the renovations himself. Then his profits will double. Instead of 1/6 [or 17%] of the cost of the house after the repair he would get 1/3 [or 33%]. This at the same time speed up the process of buying.

Abu-Waqar told Bel several ways to finance himself. Bel began to explore them.

Use of saved money

Bel picked up a house for self-purchase that needed very few repairs. The purchase took place on the same day, as he did not have to search for a buyer. The next day Bel hired an experienced builder. The builder agreed to the repair estimate and got the house fixed up in a few days. It took another week to find a buyer and sell. Bel returned the money he spent (2/3 [or 67%] of the price after the renovation) and made a profit (1/3 [or 33%] of the price after the renovation). He paid off 1/12 [or 8%] of the repaired house price his helpers. In 2 weeks, Bel made a net profit of 1/4 [or 25%] of the price of the resold house.

The profit in 2 weeks amounted to 3/8 [or 37%] of the money put in. It looked like magic. If Bel had lent that money, he would have gotten only 1/120 [or 0.8%] in 2 weeks.

Only now Bel realized the words of his mentor. Indeed, complex rules of wealth bring more profit than simple rules. In Bel's version, the difference reached 47 times!

The owner of the next house wanted to get the money for the inherited house quickly. The house needed a lot of repairs. But Bel trusted his repair estimate. The 1/2 rule gave a good profit margin in case of unexpected expenses in the repair:

Maximum Purchase Price = 1/2 of the cost after repair - Repair

The heir agreed to the price offered and received the money in two hours. He went to buy luxurious clothes and order a feast with musicians and women dancers for his friends.

After the repairs and sale, Bel made a profit of 1/2 of the value of the house after the repairs. He paid off his helpers. But the net profit in 2 weeks seemed enormous and almost equal to the money paid in.

Regular Loan

The mentor insisted that Bel study the financing of buying and repairing with other people's money.

Historical overview.

In ancient Babylon, credit utilized frequently and regularly. 4/5 [or 80%] of credits lasted up to six months.

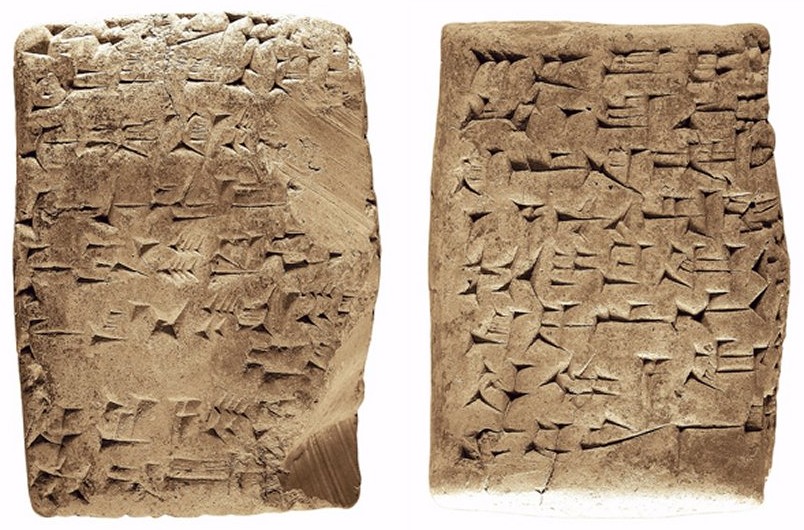

A creditor and a debtor came to the bazaar.They looked for a trading row occupied by scribes. A scribe would write the loan on a clay tablet and sign it with his name:

The creditor and the scribe checked the tablet for free with any other scribe. The other scribe would read them the text on the tablet. Then the creditor and debtor would return to their scribe. In front of the scribe, the debtor received silver or food from the creditor. The creditor received the tablet with a record of the loan.

On the specified date, the debtor and the creditor again went to the bazaar in a row of scribes. The closing of the loan took place in front of his scribe. He checked the entry in the credit clay tablet. The debtor would give the agreed amount. The creditor would break the clay plate in front of the debtor. This signified the successful closing of the loan.

Sometimes the debtor didn't pay back the loan after the deadline. Then the creditor would go to the king's court and show the tablet with the loan agreement. On rare occasions, the loan recipient refused to admit the loan. The judge called a scribe. The scribe examined the tablet. He swore by all the gods that his hand had written the loan tablet. The scribe confirmed the identity of the lender, the debtor, and the fact of receiving the loan. The judge sent royal guards to the debtor's house. They charged the loan, the interest, and all court costs from the debtor's estate.

Bel already had enough money of his own. But he began to learn how to make purchases-repairs-sales with the money of creditors.

A normal loan for a month at Babylon cost 1/60 [or 1.7%] of the loan value. Bel looked for a loan for 2/3 [or 67%] of the home's value after repairs. A one-month loan to buy and renovate a house cost only 1/90 [or 1.1%] of the value of the house after renovation. Excluding the buyers' money allowed Bel to make an additional profit that the home-buyers had previously taken for themselves. The extra profit amounted to 1/6 [or 16.7%] of the value of the house after renovation. Using loaned money cost 15 times less than going to professional home-buyers.

Usage of credit money had many advantages:

- The search for creditors passed much more easily than the search for buyers of real estate. Many Babylonians saved 1/12 [or 8%] of their income. They offered the savings on credit to other Babylonians. The rate of 1/60 [or 1.7%] per month looked ridiculous to Bel

- The lenders did not examine the houses; they only worried about the rate

- Bel could now buy houses of any value and in any quantity without his money at all.

Getting a loan had its own specifics. Unknown lenders required a mortgage. They refused to accept as a mortgage a house that needed repairs.

Professional credit

On his mentor's advice, Bel began borrowing money from old acquaintances to whom he had previously sold information about suitable houses.

A loan from professional home-buyers cost 1/30 [or 3.3%] of the money borrowed each month. This exceeded Babylon's typical loan rate by a factor of 2.

But professional buyers had absolutely no fear of mortgaging a house that needed repairs. If Bel failed to make repairs and sell within a month, a professional home-buyer will feel happy. He will take the house for himself, renovate it, and sell it.

Getting a loan from professional home-buyers took a little more time than removing silver from one's coffer. The professional buyer sent his trusted assistant to look at the house and check the estimate. Bel then made a loan agreement with a scribe and received the money.

Eased Professional Loan

Professional home-buyers placed almost all of their money into home purchases and repairs. From time to time they had spare money, which they lent for short periods of time. They preferred to lend to the same professional home-buyers. This doubled Babylon's standard rate of credit.

Over time, professional home-buyers got to know Bel well and began to trust him. Getting a professional loan simplified to the extreme. Bel would send his trusted assistant to get the money. He would go around to the professional home-buyers and show a clay tablet with the calculations. The lender didn't check the house. One verbal deal sufficed for him to provide a loan. Usually the trusted helper returned back with the money in a couple of hours. Bel could pay back the loan early, then it became cheaper.

Usually, the trusted assistant returned with the money in a couple of hours.

These same professional home-buyers turned to Bel for money when they didn't have enough money of their own. If Bel had money to spend, he would give them a loan at Babylon's double rate, too.

So Bel entered the circle of professional home-buyers.

Circle of Buyers

All of the professional home-buyers periodically gave and took loans from each other. Bel wondered who benefited in the end. Abu-Waqar explained. The Babylonian double rate loan with the house as collateral had no intention of making money. Professional home-buyers make dozens of times more on the buy-repair-sell process. The Professional loan at the Babylon double rate provided almost instant access to all the money that professional home-buyers had on their hands.

The circle of professional house buyers represented one of the few communities in Babylon, where a verbal agreement meant more than a contract fixed by a scribe. This offered many benefits:

- Bel received money for the purchase and repair of the house instantly, in any amount and without any formalities. This gave great convenience when the homeowner wanted the money on the same day

- Bel no longer had to keep a reserve of money to buy-repair the next houses. He enjoyed the freedom to inject his spare money into repairs and purchases

- Professional home-buyers had specializations in the type of homes and repairs. Often a professional home-buyer found a home that he didn't want to do the repairs on. Then he passed the information on to someone in the professional circle who specialized in that type of house and repairs.

Repair team

Repairs followed one after another. Bel hired construction workers on a permanent job. Now the repairs flowed faster and cost much less than repairs with the help of occasional builders.

His own builders knew what kind of repairs a house needed. They took turns on the same house. When a builder finished his part of the job, he would delegate the house to a builder of another specialty, and he would move on to the next house. When the last builder finished the job, Bel's assistant would put the house up for sale.

Builders trained each other in related building skills. Bel agreed with friendly, professional home-buyers to exchange builders. Each Bel builder worked several months a year with other professional home sellers and exchanged renovation experiences with them.

The actual cost of the repair, even including the cost of the estimate, decreased two times less than the price of the estimate. The increased speed of repairs reduced the cost of obtaining loans. The net profit from the transactions increased even more.

Clay Tablet 4. Renting

The funds quickly accumulated. Bel tried to manage their growth. He spent the money on hiring assistants and providing professional credit. But this contributed to an even more rapid growth of money.

Finally, Bel couldn't stand it and asked his mentor again - what to do with the money?

Abu-Waqar pointed out that Bel' gets money only when his staff works. It increased wealth well, but did not preserve it sufficiently. The mentor suggested keeping some of the renovated houses and renting them out.

Payback on houses

Now Bel found out more information before repairing:

- The rental price of the house. The rental value of similar neighboring houses served as a guide. Estimated annual rental income decreased by the time the house stayed idle looking for a tenant. Depending on the neighborhood, the idle time could vary from 1/30 [or 3.3%] to 1/15 [or 6.7%]

- Rental expenses - rent collection, house maintenance, taxes, dues to clean the canals, services of the night watchman,...

Bel determined the time when the house would fully pay for itself:

Quote: Payback period in years = Cost of house after renovation / (Annual rental income - Annual house expenses)

Depending on the payback period Bel decided what to do with the house later.

Up to 5 years. Bel kept houses with a short payback period. His builders rebuilt the house to rent out later:

- Houses with large storage rooms remained popular in the market area

- Hash houses demanded along main roads

- The houses near the caravanserais worked well as hotels for wholesale buyers. They came to the capital from all over Babylonia.

After the renovation, the house rented out. Bel hired assistants who dealt exclusively with the management of rental houses.

Over 5 years. Bel prepared homes with a long payback period to sell to buyers who intended to live in them. His builders did renovations that increased the home's appeal to buyers.

Lending of an income house

Bel liked to keep the houses to himself. It spared him the trouble of handling the silver. Keeping the silver required extra attention and protection. The property didn't fear robbers. It provided income and grew in value each year.

Soon the accumulation of silver depleted. Bel bought-renovated and sold two houses. With the profits he bought-renovated and rented out a third house. Bel liked to own houses. He wanted to keep half or even 2/3 of the houses he renovated.

The mentor pointed out to Bel that a renovated house could serve as good collateral. Bel could buy-repair-rent the house if he took an ordinary loan against the collateral of Bel's other rental houses. After repairing the house, Bel would take out a conventional loan against the house itself. He would give the money he received to the lender, who would finance the purchase and repairs.

Bel continued to obtain a professional loan at double Babylon rates only for quick purchases in one day. If Bel rented out the house after the renovation, he would take out a new loan at Babylon regular rates and repaid the expensive loan from professional home-buyers.

After a few years, the house rent of the mortgaged house fully returned the loan and the loan rate. Then Bel freely used the rent.

The constant increase in the value of Babylon's properties served as a welcome addition. The fortress walls surrounded Babylon. It could not expand:

The value of Babylonian lands and houses grew all the time.

Use of owner's money

The mentor gave Bel another piece of advice. Bel had to ask questions during negotiations with the homeowner. Why does the owner sell the house? Does he have a place to live after the sale?

If the owner had no other homes, Bel offered to sell the house, but to continue living and start paying rent. If the owner agreed, Bel freed himself from repairing and finding a tenant.

Often the proprietor already had another house. He planned to spend the money he received a little at a time. In this case, Bel offered to make a contract. Bel manages the house as his own, makes repairs, and rents it out. But the homeowner continues to formally own the house. In return, Bel agrees to pay each month a portion of the value of the house plus half of Babel's loan rate. After paying the value of the house and half the loan rate, the house becomes Bel's property. Bel reserved the right to pay the remaining amount at any time and become the full owner of the house. If the owner agreed, all Bel had to find the money for repairs. Bel sent the entire rent as a monthly payment to the formal homeowner. This expedited the complete transfer of ownership of the house to Bel.

Clay Tablet 5, Rotation

House Multiplication

The houses that Bel bought and renovated with his own money began to bring in income immediately after the renovation. The houses that Bel bought on credit paid for themselves in a few years and continued to bring in rent.

The rental house did not require much care. Every few years, it "doubled" itself. The income from the house allowed him to buy another house, make repairs, and rent it out.

Even if Bel owned one house, in 12 years, he would have several dozen houses. But Bel's assistants added one house each week for rent. Bel rapidly became a big homeowner.

Revision of houses

Each year Bel recalculated the payback period of the purchased homes. He got out of the houses with a low return on investment. With the money he received, Bel kept more of the renovated houses to test their payback period.

The rate of return on his rental houses increased.

Property for business

Bel understood better and better which houses fit better for renting. Houses for short-term living of merchants had a shorter payback period. In his 6th year Bel bought his first caravanserai.

The property used by merchants for trade paid off even more quickly. In his 12th year he bought the main market square.

By the 18th year, Bel owned half of Babylon's commercial property:

So Bel became the richest investor in Babylon.

His mentor had gone to the forefathers by that time. Bel deeply regretted his passing. In memory of Abu-Waqar, Bel decided to write five clay tablets describing his path to wealth.

The remainder of the 5th tablet lists Bel's main commercial property and its income. Bel's total income amounted to 360 talents of silver [or 1,296,000 silver shekels or 10.9 tons of silver] per year.

Film version of the book

Cambridge Department of archaeology filmed stories from life in ancient Babylonia.

An example of this is the parable film "The Poor Man of Nippur." The film was acted by Assyriology students and other members of the Cambridge Mesopotamian community. The storyteller and actors speak in ancient Babylonian. Please enable subtitles:

Advertisement

There is a good opportunity to screen the book "The richest investor in Babylon" in ancient Babylonian language.

If you would like to sponsor the film "The richest investor in Babylon", please contact us.